Successful Cloud transformation embraces new ideas and deploys flexible technology for data analysis, collaboration, and customer focus. Digital transformation with the Cloud is essential to keep pace with the changing business and market dynamics. Cloud technology is now a part of the playbook for most enterprise IT departments, with Cloud enabling digital transformation by creating and modifying business processes, culture, and customer experience. Cloud adoption can be challenging for businesses without the right strategy. Unaligned efforts often fall flat for most organizations due to a lack of planning and a poor understanding of business objectives.

Starting Your Cloud Journey The Right Way – Steps To Cloud Transformation

A cloud journey enables companies to seamlessly move their applications and workloads to the Cloud. A strategic approach that avoids disrupting current processes is the right path to a successful Cloud journey and transformation. Here are a few essential steps that will guide you in your cloud journey:

1. Adopt A Three-Pillar Approach.

Business, operations, and technology are the three core pillars of any company. A strategic approach that addresses these three pillars is integral to getting maximum value from cloud adoption or migration. Identifying business domains that can realize the full potential of the Cloud to increase revenues and improve margins, choosing technologies in line with your business strategy and risk constraints, and implementing operating models oriented around the Cloud will enable companies to drive innovation and achieve sustainable, long term success with cloud transformation.

2. Prioritize These Questions Before Crafting Your Cloud Transformation Strategy.

Before you embrace a cloud journey, answering these questions will help clarify your security strategy and establish a roadmap for your cloud journey. Here are a few essential questions you need to answer:

⦁ What is your motivation to invest in Cloud?

⦁ What challenges will the cloud address?

⦁ Will customers derive tangible benefits from switching to the Cloud?

⦁ What long-term benefits are you looking to achieve?

⦁ How will the cloud impact business and organization culture?

⦁ How will cloud transformation impact current business processes?

⦁ In what ways have you integrated technology throughout your company? What are your expectations?

⦁ Do you have an existing strategy for successful cloud adoption and migration?

3. Navigate The Cloud, One Step At A Time.

Cloud transformation can be complex, but following certain best practices can ensure a successful journey. Dividing the cloud migration process into planning, migration, and ongoing cloud management will help achieve integrated transformation. Let us look at each of these steps in detail.

Planning

The planning process consists of three main steps: Discovery, Assessment, and Prioritization. Discovery refers to identifying all the assets in your technology landscape. Assessment includes evaluating the suitability of on-premises apps and services for migration. The prioritization process determines which applications and services should be migrated to the Cloud to establish a timeline. Let’s look at the three steps: discovery, assessment, and prioritization.

1. Discovery

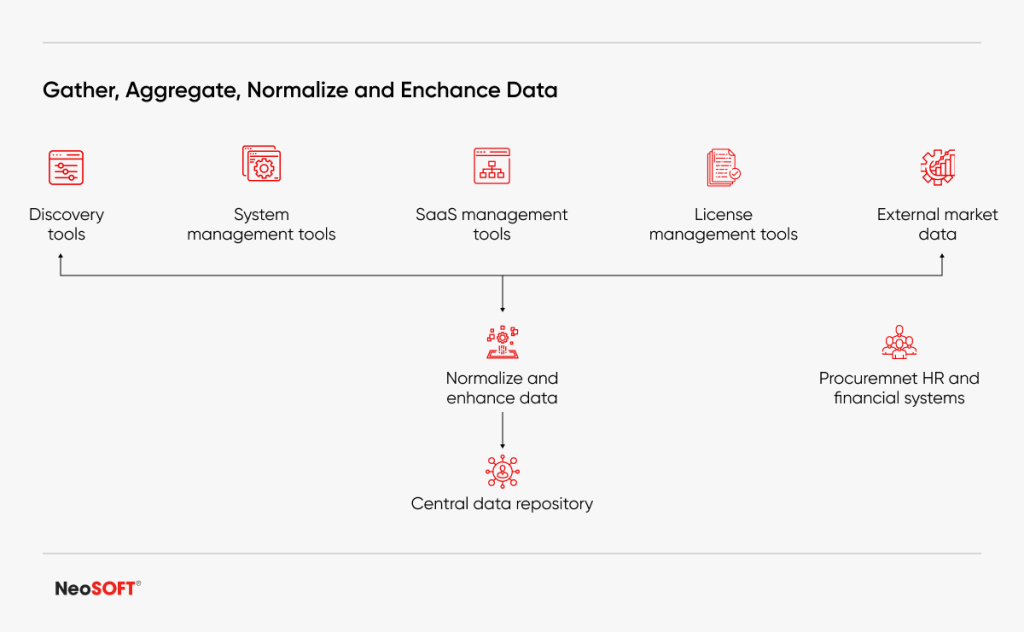

A thorough understanding of the on-premises environment is crucial before migrating to the Cloud. Many businesses still rely on traditional IT architectures, with applications designed for on-premises use. An accurate overview of all the on-premises applications is essential for effective migration planning. The IT landscape’s hardware, software, relationships, dependencies, and service maps need careful evaluation during discovery—any potentially hidden SaaS apps considered to ensure a clear understanding of the technology landscape.

Track assets to delve deeper into more critical details about them:

⦁ Ownership details

⦁ Asset usage patterns

⦁ The cost incurred for the assets

⦁ End-of-life or end-of-service dates

⦁ Software licensing terms, conditions, and renewals

⦁ Application compatibilities

⦁ Security vulnerabilities

As illustrated in the figure below, most of this information is available in your company’s internal sources, such as system & license management tools, procurement systems, human resources systems, and internal sources. At the same time, you can obtain information about EOL and EOS dates, compatibility issues, and security vulnerabilities from external sources. Such information contains clues that allow organizations to plan their cloud migration journey effectively.

The next step is to assess which apps and services need migration to the Cloud. The key factors to consider when determining the suitability of existing applications and cloud providers for migration are as follows:

2. Assessment

The next step is to assess which apps and services need migration to the Cloud. The key factors to consider when determining the suitability of existing applications and cloud providers for migration are as follows:

⦁ The level of effort needed to migrate an app or service.

⦁ Apps and services that don’t require migration.

⦁ Architecture or security concerns and business impact or customer impact.

⦁ The total cost of ownership of on-premises apps or services.

It is essential to determine which applications fit better into the Cloud environment. When migrating apps and services to the Cloud, key decision-makers need to be sure of the benefits it will bring in the long term. Companies must evaluate the cost of running the apps on the Cloud compared to keeping them on-premises with assessment tools.

3. Prioritization

This phase prioritizes the apps that must move to the Cloud first. How do you determine which apps must migrate first and which can wait? Let’s prioritize.

⦁ Start your migration process by focusing on less complex apps.

⦁ Choose apps that will have a low impact on the business operations.

⦁ Give priority to internal-facing applications before the customer-facing application.

Businesses can opt for migration for technological reasons. Migrating an app with heavy storage requirements makes sense only if its storage usage is near capacity and demands hardware upgrades on-premises.

Cloud Migration

Consider the changes migration will bring to your business model. Before migrating the assets, they should share the data acquired in the planning and assessment stage with the stakeholders and IT teams. Hence, everyone is well aware of migration’s impact on the business. Here are a few steps outlined to maximize the chances of successful cloud migration.

1. Plan your Cloud migration.

Consider the total cost and migration structure and evaluate the service provider for your migration beforehand. Establish the migration architect role to design strategies for data migration and define cloud-solution requirements. A migration architect plays a critical role in executing all aspects of the migration. Determine the level of cloud integration (shallow cloud integration or deep cloud integration). Choose whether to go single-cloud or multi-cloud, depending on your business requirements. Establish performance baselines well in advance to diagnose any problems and evaluate post-migration performance.

2. Prioritize Cloud Infrastructure security.

Security is a significant concern for every business when switching to Cloud. An impactful analysis is integral to understanding the security gaps in the cloud transformation journey. Companies increasingly rely on machine data to gain insights into security vulnerabilities and ensure apps and services run securely. Picking the right cloud hosting platform is crucial to ensure the longevity, stability, speed, security, and cost-efficiency of the digital assets you have planned for cloud enablement.

3. Set objectives and key results.

Before starting the migration process, businesses must establish objectives and key results (OKRs). Objectives and key results help determine whether the migration has benefited the organization. Development productivity, user and developer experience, stability and security, and speed to market/delivery are a few of the critical metrics businesses must measure to ensure a successful migration.

4. Set up compliance baselines.

Businesses need to adhere to a set of rules and regulations when planning their migration. Compliance rules keep evolving in response to the threat landscape, and companies should ensure continued compliance by investing in the proper security controls and configurations.

You can put your cloud migration plan in motion for one or more assets after evaluating factors such as urgency, adaptability, and ease of execution. Businesses often consider metrics such as the total number of users, device count, location, interoperability, business continuity, and data integrity.

Tips for Successful Cloud Migration

Listed below are a few tips businesses can follow to ensure a future smooth migration:

A cloud strategy should align with your business strategy and business operations.

Creating a cloud strategy that aligns differently from your overall business strategy could benefit your ROI. Your cloud migration strategies should support and facilitate the implementation of business strategies. Focus on more than just the IT aspect of your business. Ensure the chosen business verticals benefit from your cloud strategy.

Assess Cloud-related risks.

Businesses must assess the five cloud-related risks such as agility risk, availability risk, compliance risk, security risk, and supplier risk. Evaluating these risks ensures sound cloud deployment decisions for your business. Weighing the risks against the benefits offers better clarity on the post-migration performance of the company.

Consider different Cloud migration strategies.

There are different approaches to cloud migration, and you can select the one that best suits your needs. Rehost, refactor, repurchase, re-platform, retain, and remove are the six cloud migration strategies businesses can implement.

Get rid of data silos.

Data silos present multiple risks and impede performance. Businesses should establish a common data platform across clouds to eliminate silos. A unified view of the Cloud with a single platform ensures a seamless user experience while eliminating the need to refactor for separate vendors when moving data from one Cloud to another.

Utilize Cloud staging.

Cloud staging refers to moving elements of end-user computing to the Cloud. It helps users transform desktops with centralized cloud-based storage. Businesses choose between maintaining existing desktop types alongside a new platform or migrating their users entirely to the new platform. With cloud staging, users can migrate to another desktop with zero downtime for maximum productivity.

Create a Cloud-first environment

Creating a cloud-first environment will ensure your business reaps the full benefits of cloud adoption. To adapt to the cloud environment workforce must be trained. The Cloud is a powerful tool for digital transformation and an inseparable component driving innovation for your business. By utilizing the Cloud’s scalability, flexibility, and advanced features, companies are successfully transforming their operations, optimizing their resources, and unlocking new growth opportunities.

Execute effective testing

Testing gives insights into whether the migration will produce the desired results. Testing enables you to simulate real-world workloads to understand slowdowns and outages as you migrate across load scales.

Ongoing Cloud Management

Ongoing cloud management refers to managing the applications and services on the Cloud as soon as the migration is complete. Cloud migration is not a one-off activity. After migration, businesses must operate and optimize in response to changing business requirements.

Cloud management begins with the migration of the first workload. Automation tools play a critical role in managing cloud-based workloads. Cloud management is essential to ensure optimal resource management, security, and compliance in this fast-paced environment.

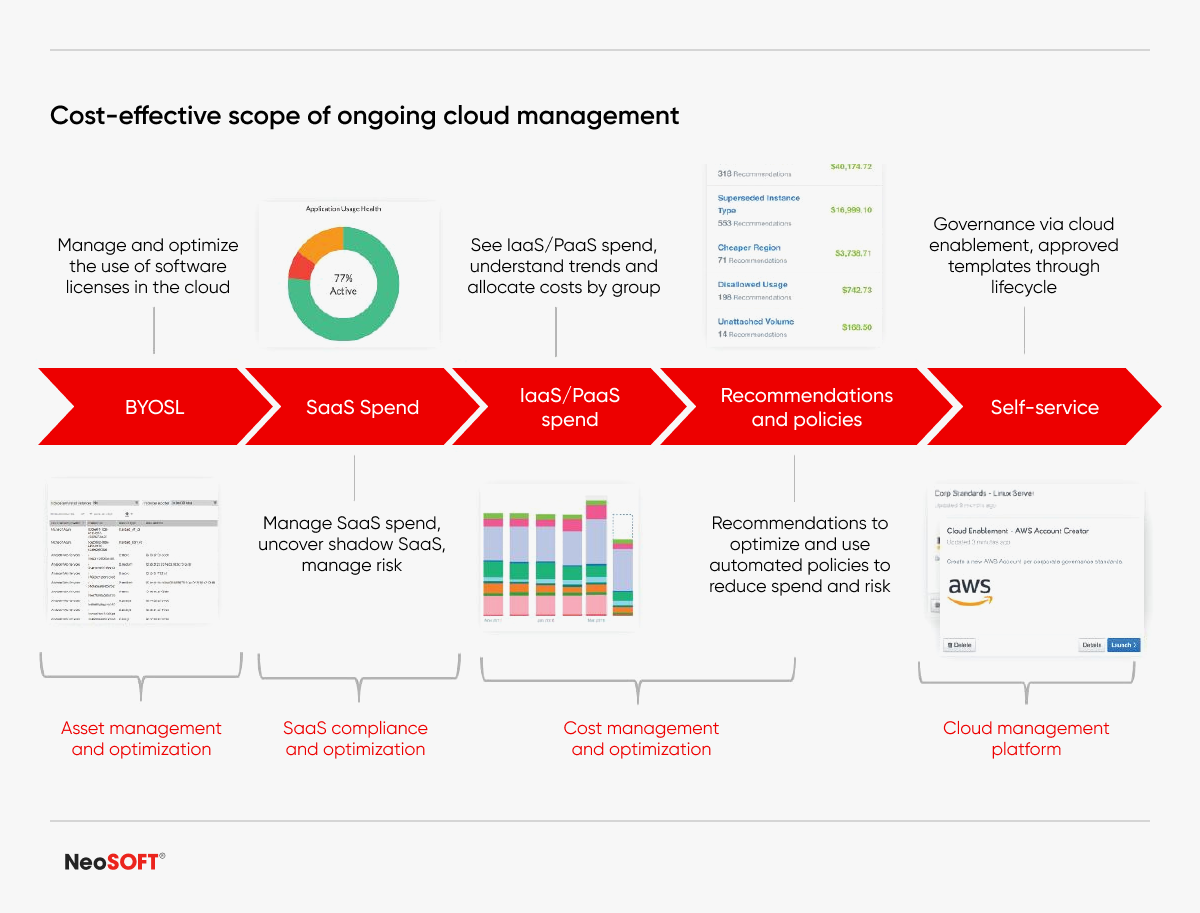

An overview of the cost-effective scope of ongoing support for cloud management consulting might help understand its need better.

We list below the top cloud challenges and tips to curb them in your ongoing cloud management activity:

1. Cloud governance and compliance

Governance is crucial in maintaining the alignment between technology and business and ensuring compliance with corporate policies, industry standards, and government regulations.

⦁ Set standardized architectures that comply with corporate versions, patches, and configuration guidelines.

⦁ Capitalize on reusable templates to deploy standardized architectures and orchestrate infrastructure and services across public clouds.

⦁ Orchestrate ongoing operations such as monitoring and performance optimization; alerts, notifications, and escalations; and self-healing capabilities.

⦁ Automate compliance with governance frameworks

When individuals and departments acquire SaaS apps without the knowledge of Central IT, such apps may not comply with the rules and regulations as they are outside the purview of the IT governance framework. Therefore, central IT must be involved in technology selection to align the assets with the compliance requirements. Implementing the right governance tools will enable companies to automate compliance and define standardized architectures that comply with corporate guidelines.

2. Optimizing spends

Optimizing cloud spending is a significant challenge facing modern businesses. Cloud resources used optimally achieve more substantial cost savings. Ongoing cloud management ensures the efficient use of cloud resources at reduced costs. Best practices include:

⦁ Eliminating apps with overlapping functionality.

⦁ Identifying unused apps.

⦁ Implementing the latest tools to identify areas with potential for cost savings.

⦁ Leveraging cloud-based automation to increase productivity.

3. Strengthening security

Decentralized decision-making is a significant contributor to weak security. All stakeholders and employees involved should be equally aware of the importance of safety and the best practices to ensure maximum Cloud security. There are different tools that businesses can employ to improve security in the cloud environment. These tools will send alerts for misconfigured networking, facilitate role-based access, maintain audit trails that track cloud resource usage, and ensure integration with SSO and directory services for consistent access to cloud resources.

NeoSOFT has been fueling the shift towards cloud enablement for businesses across industries.

Developed AWS Cloud Infrastructure and Containerized Applications

NeoSOFT provided a cloud architecture solution design and VPN tunneling for authorized access to sensitive data. This mechanism adds an extra security layer to the stored data. Our developers utilized an OS-level virtualization method for application containerization to deploy and run distributed application solutions.

Impact: 70% Increase in Data Efficiency

Integrated IoT and Cloud Computing for a Customized Home Automation System

Our team of expert cloud engineers leveraged automation and cloud tools to develop a cross-platform application that integrated a simple and intuitive design, offering seamless access to smart home devices. The application’s user-friendly interface boosted engagement by providing greater control over security, energy efficiency, and low operating costs. Enable users to monitor, schedule, and automate all their smart devices from one location.

Impact: 25% Increase in Download Speeds

Engineered a Robust Cloud-Based Web App for the World’s First Fully-Integrated Sports Smart-Wear Company.

Our Cloud engineers empowered the client with cloud computing and data management tools to construct a website featuring distinct modules for the admin, affiliate marketing, and channel partners. The app efficiently manages country-specific distribution, influencer-based product promotion, and user data access. Advanced analytics integration also provided real-time sales reports, inventory management, device tracking, and production glitch reporting.

Impact: 30% Increase in Operational Excellence

The Road to Cloud Success

Navigating the journey and transition toward cloud transformation can be challenging. However, many enterprises have moved to the Cloud in response to challenges they have experienced, like unexpected outages, downtime, data loss, lack of flexibility, complexity, and increased costs. Businesses that embrace cloud transformation may retain their competitive advantage. Cloud migration allows enterprises to move from a Cap-Ex-based IT infrastructure to an Op-Ex-based model.

The right people, processes, and tools can facilitate a smooth cloud transformation journey. Businesses can witness sustained results only if technology execution capabilities are up to the task. The key to cloud transformation success is to select a migration model that aligns with economic and risk constraints. The company should clearly understand its risk appetite and business strategies when making cloud transformation decisions and evaluating its IT capabilities.

The global enthusiasm around open banking has been soaring high as it sets a pace for the industry 4.0 to transform systematically through digital change and disruptive innovation. The transformation is just not limited to how banks would eventually evolve, but primarily aims at introducing value-added benefits for the customers and building a secure value chain.

Let’s dive into the concepts of open banking and understand the drivers that are fueling this innovation, the challenges and threats it poses, and how banks and other players plan to transform and develop new revenue models through the open banking channel.

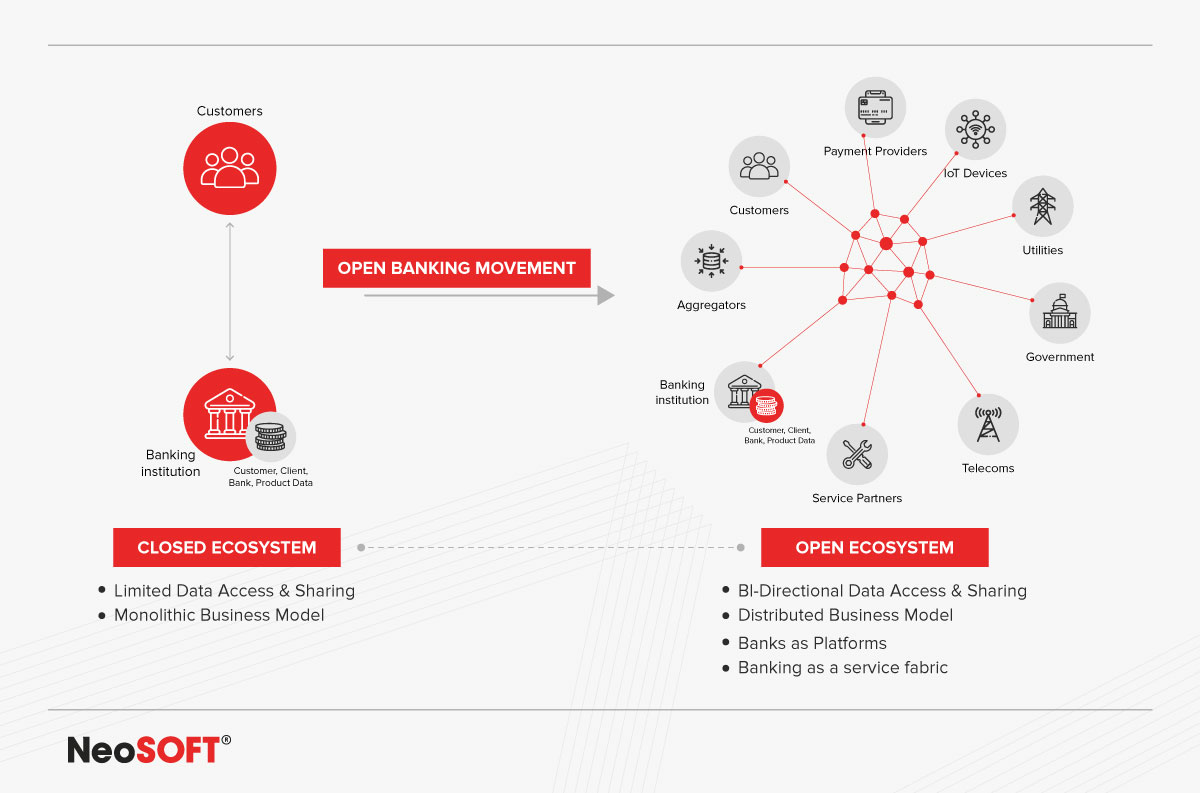

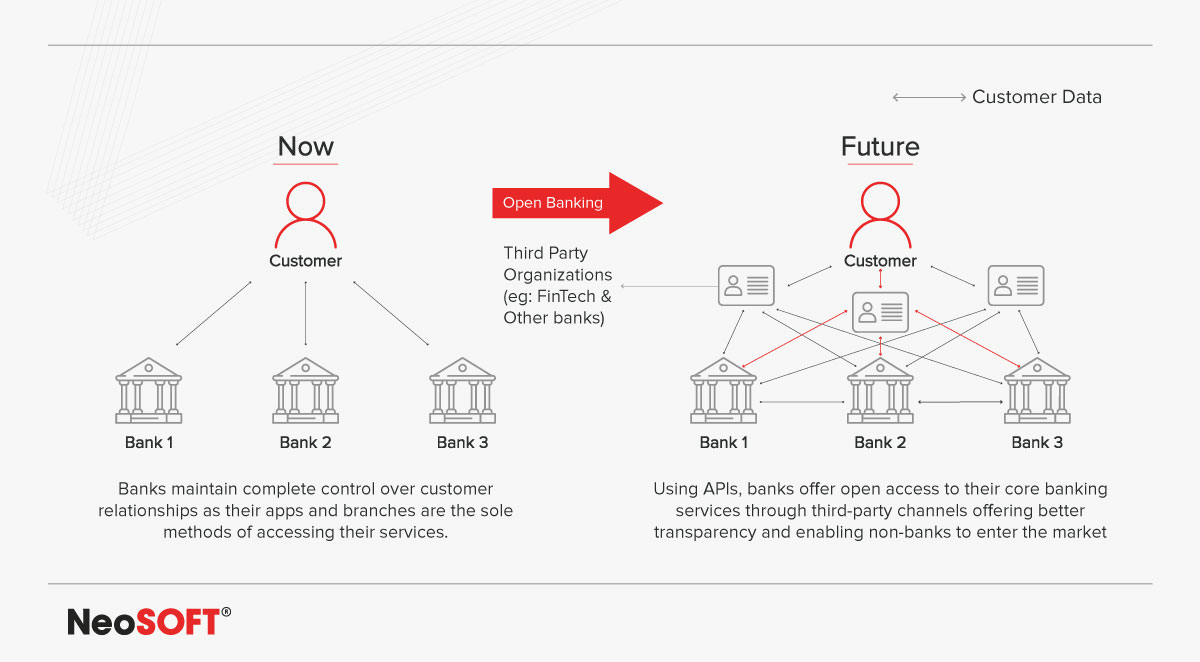

What is Open Banking?

Open banking, also known as ‘open bank data’, is a platform-based approach that is destined to stay and evolve. It is a banking practice that provides third-party financial service providers with open access to consumer banking, transaction, and other financial data. The consumer data is captured from banks and non-bank financial institutions through the use of application programming interfaces (APIs).

The Evolution of Open Banking

Financial institutions, since their inception, have been collecting precious information about their customers and their transactions, with little or no knowledge of how to harness this data to its effective value.

Today, financial institutions leverage the data to narrow down customers’ preferred choices and this includes everything from their favorite restaurant or coffee shop to which shops they buy most of their shirts. Financial institutions also capture non-consumer data known as meta-data from cash machines, branch locations, number of loans, mortgages, different account types, and volume of transactions. With all this data captured in heaps, it becomes easier to analyze customer preferences and suggest relevant products and services that could be of their interest.

Due to an increase of around 50% in access to additional customer data and an approximate 70% decrease in time to market, open banking is without a doubt garnering the most interest within the fintech industry.

If we think about the short term alone, open banking is expected to increase financial institutions’ revenue by at least 20%-30%. These numbers are jolting the fintech industry towards renewed innovation of banking and payment services, making it easier and more accessible for customers.

Conventional Banking Vs Open Banking

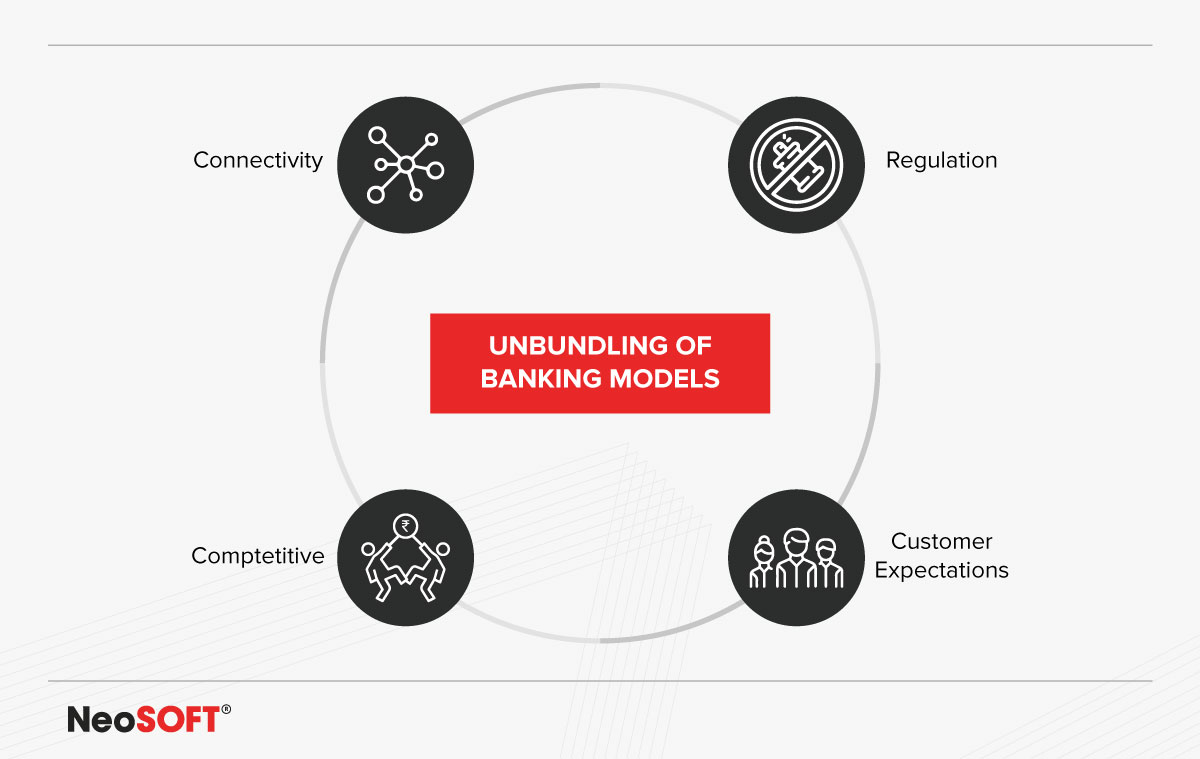

Driving Forces Behind Open Banking Adoption

Due to the global pandemic, the past few years have been quite challenging for financial institutions. This situation also built opportunities to innovate and introduce solutions that had the potential to drive a positive impact on their future profit goals.

1. Changing Customer Behavior and Expectation

Newer and older generations such as Generation Z or Generation Alpha, have distinctly different behavior and requirements, pushing financial institutions to rethink their process for creating and selling their products and services to them.

For instance, a bank has to consider whether the product or service they offer satisfies the customers’ needs or not. The shift from a product-centric approach to a customer-centric approach is important. This mindset has caused financial institutions to rethink and upgrade their offerings by keeping customer experience at the core of the product development process. Moreover, these days customers enjoy an unprecedented level of market transparency, and their satisfaction level goes beyond accepting a limited choice of products offered by their main bank. With exposure to frictionless user experiences, they can now quickly differentiate between a good and bad CX, and are now not in a state to accept anything mediocre.

2. Technology Fueled Innovation

Radical innovation in digital technology, exponential growth in smart devices, and the shift to instant payments, have opened new opportunities within financial services. Spurred on by the growth of APIs, they have now become the foundation of the entire open banking system. The integration of cloud-based platforms has further enhanced the agility, flexibility, and scalability of financial institutions’ abilities. Additionally, advancements in exponential technologies such as AI, real-time analytics, machine learning, and blockchain have further improved processes, services, and products across all levels.

3. Evolving Regulations

Governments across the globe have been ushered into taking a proactive approach to the “democratization” of financial products and services. Nudged on by EBA in the EU after the adoption of PSD2 in 2015, formally ushers in the concept of open banking. Regulation breeds innovations and naming the concept as ‘open’ denotes its explicit policy goal that the concept must be considered and adopted across all financial institutions. Compelling banks to make their proprietary data available to third-party providers.

4. Increased Competition

A large number of organizations – backed by technology giants like GAFA (Google, Amazon, Facebook, and Apple) – have entered the financial services market. These fintech organizations are providing quicker payment solutions, with seamless integration of cards, e-wallets, and other payment options fueling competition with the banks. As a matter of fact, these organizations are more ready and actively preparing to offer their services within the open banking ecosystem, further ramping up competition with banking institutions.

Unbundling of Banking Models

How Open Banking Will Take the Front Seat in the Financial Ecosystem

Currently, the ‘open revolution’ market consists of both: established financial institutions and new players. The range of applications begins from a ‘minimum approach’ that permits third-party access using APIs for the purpose of sharing selective data to ‘maximum implementation’ facilitates the integration of diverse functionalities by leveraging the Banking-as-a-Service platform (BaaS).

‘True’ open banking goes beyond the exchange of information and impacts the core elements of financial service providers including established processes and legacy core banking systems. They possess tremendous potential and allow players with varying needs to connect, therefore benefiting different bank types and the entire financial industry as a whole. The customers too benefit as they gain access to a wider range of products at a single touchpoint rather than reaching out to multiple service providers.

For some product categories like mutual funds, mortgage loans, or structured products, incorporating third-party products has been a common practice for banks for many decades thus far. This concept has also been applied to deposits, one of the most widely used products by bank customers and a major source of funding for banks.

Flexibility and a More Complex Competitive Environment

Driving Value for Stakeholders

The open banking ecosystem is geared toward a holistic benefit approach that considers its customers as well as the industry stakeholders. Outlined below are a few instances of value created by the innovation open banking platforms have adopted.

1. Flawless User Experience

Due to the potential convergence of open banking and artificial intelligence, user experience is undergoing an incredible digital transformation. The continuous influx of data across several sources enables service providers to determine the exact customer sentiments and requirements resulting in highly personalized financial offerings. Several tedious procedures are also expected to become simplified and automated. Through banking APIs, fintech firms offer users the opportunity to improve their financial lives through financial planning capabilities and insights based on their own data. Essentially, opening banking enables banks and similar financial institutions to create a unique financial profile for each customer according to their financial data. Allowing them to predict their consumption patterns and behavior to execute product customization more efficiently.

2. Real-Time Payments Facilitating Easier Treasury and Cash Management for SMEs

Open banking facilitates near-instantaneous payments, as third-party providers can bundle all payments within a single digital interface. Typically, SMEs don’t have their own treasury departments, unlike their bigger counterparts. Real-Time Payment (RTP) transforms treasury management services, driving value for SMEs through increased visibility of their cash flows and liquidity positions. RTP also speeds up the Peer to Peer (P2P) payments, bill payments, and e-commerce payments ecosystem.

3. Data Sharing Prompting Product Innovation and Financial Freedom

Open banking ensures that banks only share their customer’ data with authorized third parties. This will lead to the development of better financial products as organizations can leverage the data to extract customer insights and subsequently become more innovative and customer-centric.

4. APIs Enhancing Cross-Selling and Cost Optimization Opportunities

Open Banking offers banks the opportunity to blend product and service features offered by third-party providers to create their own offerings using APIs as a plug-and-play model. Tying together such readily available services from third-party providers and vice versa, banks can quickly improve customer service, boost customer loyalty, create new revenue streams, and decrease bank operating costs. Moreover, banks can mitigate the risk and expenses of experimenting with newer products simply by adopting the plug-and-play model of integrating APIs of third parties along with their core products on their digital platform.

5. Data Transparency

The need for building transparency might seem obvious, but each platform and disruptive technology comes with its own story and unique set of challenges. For open banking platforms, these challenges have given credence to the regulatory and similar competent authorities to focus on the need for building transparency by ensuring that the customers’ interests and rights are at the heart of all focus areas.

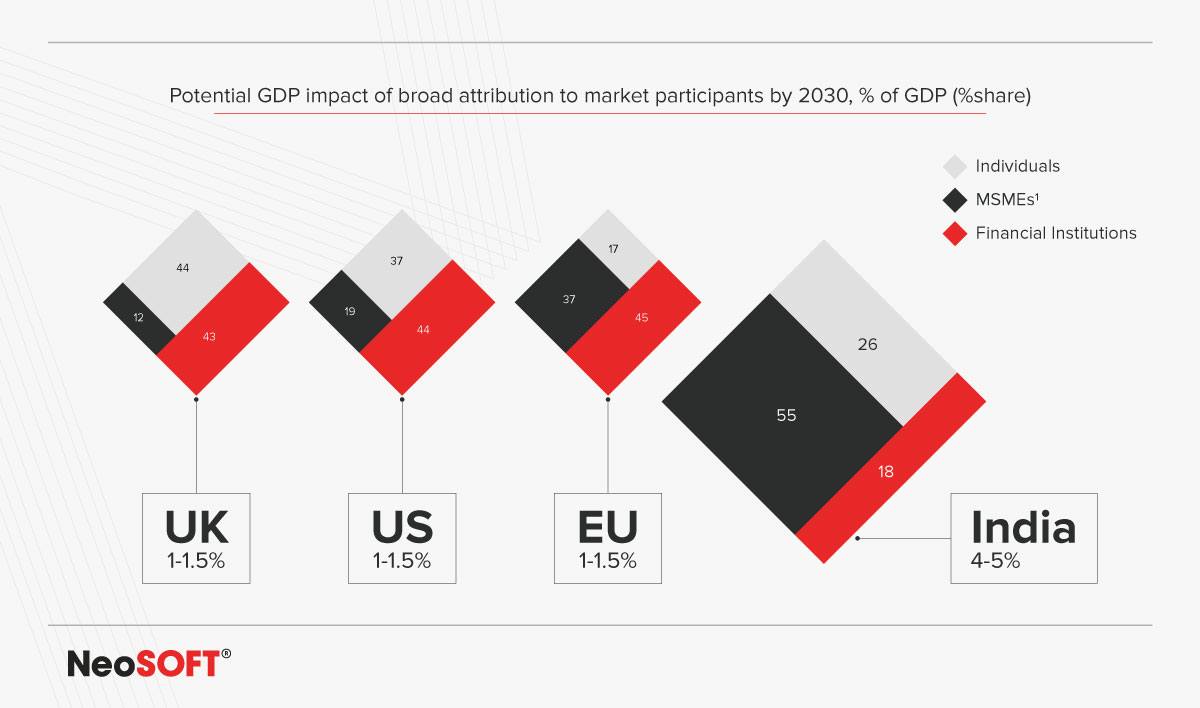

The potential impact of open financial data on GDP and how it varies according to different regions.

Risks and Challenges Banks Need to Consider to Succeed in the Open Banking Ecosystem

Although the advent of open banking has been largely positive for the financial sector, it has also opened up several new challenges and risks for banking institutions. Many of these will have far-reaching consequences for their business prospects, possibly reaching the point of existential crisis.

Let’s consider some of the key points:

1. Rise of New Competition

Leading banks are now being challenged by pure digital entities like GAFA. These fintech are attracting customers in heaps by providing unbundled, innovative, and engaging financial products and services. Meanwhile, many leading banks are still relying upon legacy systems, and if the threat is not addressed soon, will risk the prospect of losing their market share, greater customer churn, and increased pressure on margins.

2. Data Security

Sharing financial data through APIs to third-party providers bears the inherent risk of data security and breaches. The absence of industry-wide technical standards and data sharing protocols might leave operating processes vulnerable to security breaches and fraudulent activities. Using complicated interconnections of data access, banks need to invest heavily in security initiatives and risk mitigation, which often heavily impacts their bottom line. At the same time, banks cannot afford to miss out on the potential revenue generated by these data streams within the open banking ecosystem.

3. Risk of Commoditization

Due to open APIs, leading banks will face the risk of being commoditized. Reason: The elimination of several existing barriers to switching accounts and shopping around for other products based on price only. Banks face the likelihood that a significant portion of their customer base might turn to the convenience of digital aggregators, resulting in the migration of their accounts and the profit pools tied to them.

Sustaining Long Term Growth Through Business Transformation

The business transformation gained from adopting a platform-based open banking ecosystem will foster an environment that goes beyond incremental change and value delivery. It incorporates strategic choices that affect financial institutions’ growth – how they operate and the kind of improvements they can expect going forward.

Listed below are a few imperatives for creating long term growth for financial institutions:

Improve the existing range of offerings by reinforcing the core through collaboration with third-party providers.

Build new value propositions by incorporating customer needs and financial position within service integration. This will allow credit scoring, pricing of loans, and other products to be refined and curated on a more personal, almost one-to-one basis.

Collaboration and partnership between banks, third-party providers, and merchants will create a marketplace-like ecosystem. Allowing financial products to be bundled along with other non-financial products leads to newer cross-selling opportunities.

Diversify the traditional service portfolio by building strong API portfolios, boosting engagement with the developer community, and promoting cross-collaboration across marketplaces.

Concentrate on the adoption of the Banking-as-a-Platform (BaaP) model with an API-enabled network of partners, allowing core services to be bundled with third-party providers – facilitating advisory, business management as well as traditional banking services.

It is clear that open banking is set to fundamentally alter the financial service landscape through innovative services and new business models. The emergence of fintech will bolster collaboration as well usher in a new ecosystem that will change the role of banks significantly. Also, there are several issues surrounding regulation and data privacy causing a varied approach toward implementation across countries. However, irrespective of their geography, the momentum gathered by open banking is high, requiring banks and other fintech institutions to increase collaboration with each to ensure success within this new emerging ecosystem.

NeoSOFT’s Use Cases

Financial institutions across the globe leverage our expert open banking capabilities to enhance their customer experience, boost innovation, and improve adherence to data security and governance. Take a glance at how our solutions have impacted clients…

Helping a leading bank enter new markets, extend its customer base and increase the volume of transactions.

NeoSOFT was tasked with helping the bank meet changing customer expectations by leveraging alternative tech solutions that help the client address their money management requirements. Our engineers devised solutions to establish fintech partnerships, facilitating an increase in account acquisition through APIs and growth in transaction volume

Facilitating high-velocity innovation through banking APIs and an API management platform for a renowned financial services provider.

The client wanted a defined organization-wide API strategy that aligns with overall business goals while maintaining autonomy. Our solutions enabled the client to build a single developer portal for all their branches to provide insight into API adoption patterns. Our team of engineers were also able to balance organization-wide governance and cross-geography oversight for better management.

Amplifying the API Management platform for one of the largest and most popular BFSI clients.

The requirement was to lay the foundation for loyalty-driving open banking services, increase compliance and accelerate internal integration to a secure API platform. Our solutions enabled the client to adhere to its regulatory obligations while delivering an innovative customer-facing service. Additionally, it also delivered a notable uptake in operational efficiency across the organization.

For more than half a century, banks have been at the frontier in embracing automation and introducing digital systems to gain operational excellence. Today, their demands have grown and banks now look beyond their legacy core banking systems that have been, to date, leveraged for conventional services such as opening up new accounts, processing deposits and transactions, and initializing loans.

Digital innovations are disrupting the marketplace and the continuous evolvement and spurt of technologies have now radically put these legacy systems back in the race. New players are beginning to enter the market without the burden of outdated technologies.

The rise of Fintech startups, teeth-gritting competition, and the fast-paced digital momentum have exponentially elevated consumer expectations and have forced banks to modernize their digital assets.

What is Core Banking Modernization?

Core banking modernization is the replacement, upgrade or outsourcing of a banks’ existing core banking systems and IT environment, which can be scaled and sustained to perform mission-critical operations for the bank, empowering it to harness the power of advancements in technology and design.

Banking Yesterday, Banking Today, and Banking Tomorrow

The core banking solutions of the future shall accommodate global perspectives so that it gets easier for the banks to deploy systems across multiple geographies. In comparison with the legacy systems, these new systems shall be more lean, scalable, process-centric, economical, and deployed over the cloud which shall empower banks to be agile and meet the changing business requirements.

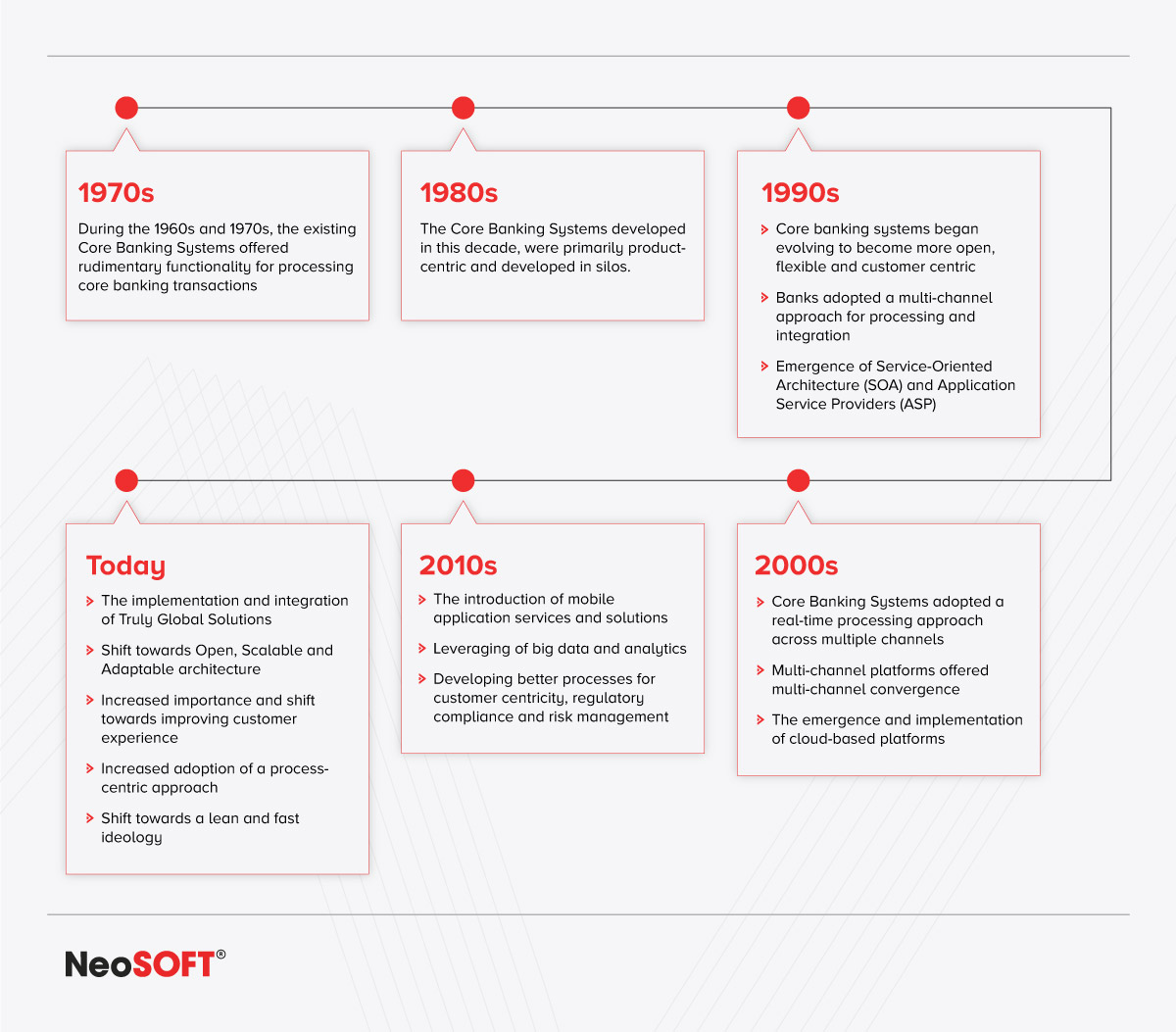

EVOLUTION OF CORE BANKING SYSTEMS BY DECADE

In pursuit of embracing innovative features and scaling customer experience, the banks are at a disposition where they seem to be keen on accepting data-driven and cutting-edge technologies, and lean and agile processes. This transformation is disruptive and banks need to strike the right balance between revitalizing their core systems vis-à-vis creating new products and services to thrive in a digital society.

To address the challenges of the near future and the next normal, it is necessary to conduct a thorough assessment of the current core banking platform and external environments. Modernizing legacy applications is a critical process and it requires a disciplined and well-thought approach. Banks will need to understand whether a full replacement or a systematic upgrade will offer a better value-to-risk ratio.

Modernization Objectives and Drivers

Core banking modernization is driven by the need to respond to internal business imperatives such as growth and efficiency as well as the external ones such as regulations, competition, and customer experience expectations.

As new banking products, channels, and technologies enter the marketplace, the complexity and the necessity to modernize old legacy core banking systems becomes more crucial. The internal and the external drivers pushing the banks to transform are worth consideration.

Internal Drivers:

Product and Channel Growth

Managing high volumes of product-channel transactions and payments demand scalable and sustainable modern core banking systems. The introduction of ever-increasing custom solutions/products to satiate a wide segment of customers which is further amplified with multifarious channels creates an opportunity for banks to re-strategize their old digital assets.

Legacy Systems Management

With technologies that had been used to build the legacy systems getting obsolete, finding resources to manage these outdated systems also gets difficult. Moreover, introducing new technologies into the systems benefit the banks in staying relevant, achieving flexibility and cost-effectiveness.

Cost Reduction

Modernizing core applications involves consolidating the other stand-alone applications that stand peripheral to the core. This subsequently optimizes the overall cost and helps banks in reducing the high maintenance costs associated with legacy systems.

External Drivers:

Regulatory Compliance

It is imperative for the banks to enhance their IT infrastructure and operations in order to comply with increasing regulations such as Basel III, Foreign Account Tax Compliance Act (FATCA), and the Dodd-Frank Act, all of which are aimed at 1) Enhancing risk management 2) Governance procedures and, 3) Improving transparency of banking operations that also involves customer interactions.

Increasing Competition

The competition pressure compels banks to innovate and embrace new core banking platforms. The new entrants in financial services are speculated to give banks a tough run and start questioning their purpose of existence.

Customer Centricity

Customer experience is a derivate of many components and banks need to re-strategize their positioning. Moving from a product-centric to a customer-centric approach is highly necessary. Focus on customer service, relationship-based pricing, and digital experience shall be the crucial elements in the transformation journey.

OBJECTIVES OF CORE SYSTEMS TRANSFORMATION

Best Practices in Core Banking Modernization

Evaluate Technical Debt: Banks should be able to closely identify and calculate their technical debt so that they can properly prioritize the debt and its impact on the legacy system processes. To get an accurate assessment, banks will need to factor in the prospective cost of adding or altering features and functionality later.

Outline the Organization’s Objectives and Analyze Risk Tolerance: When going for legacy system modernization, the bank must assess various business variables like customer satisfaction levels, modernization objectives, cost savings, business continuity, and risk management. These thorough assessments will help to provide context for the selection of the most efficient and effective modernization approach.

Choose Futuristic & Advanced Solutions: Technology refinements are taking place at an unprecedented scale, which demands organizations to be agile in the adoption of future technologies. For this, it is critical to build solutions that support future adaptability.

Define the Post-Modernization Release Strategy: The most crucial modernization practice is to create a follow-up plan that includes successful training of employees, ensuring systematic and streamlined process, timely update schedule, and undertaking other maintenance tasks.

Legacy modernization will empower traditional banks in performing a wide range of modern banking services which shall be robust and scalable. Moreover, the digitalization of traditional banks shall address the changing needs of customers through seamless digital services and drive excellent customer experience.

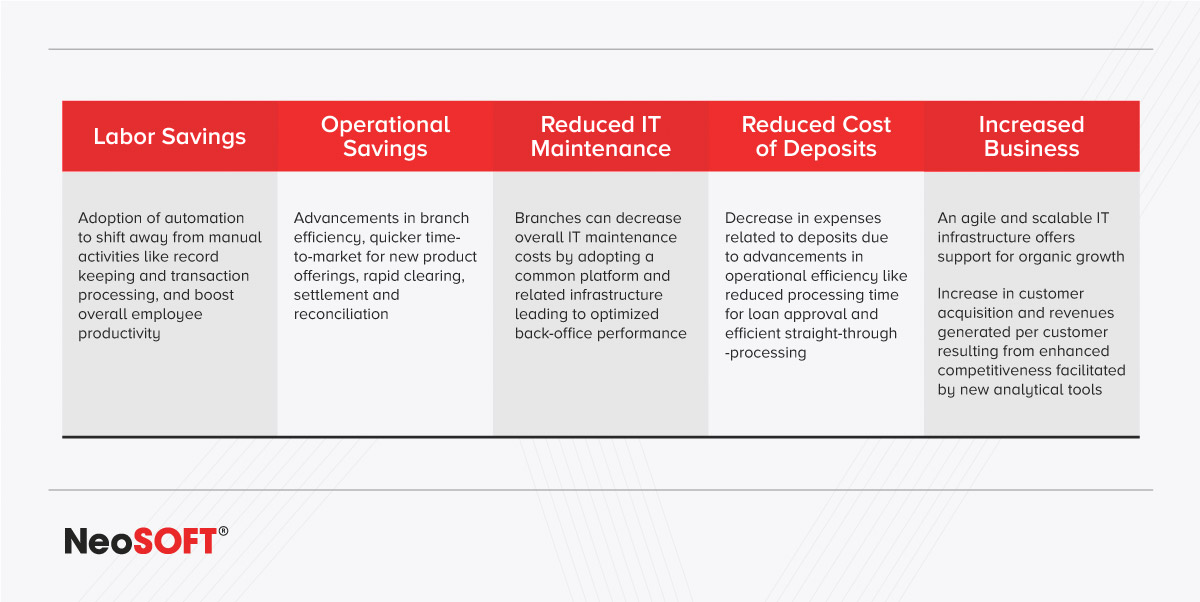

Legacy Modernization Benefits

Faster Customer Onboarding: Deploy cutting-edge technologies such as Artificial Intelligence, Blockchain, Data Science, etc. to speed up the customer onboarding process. Remember, that the customer experience is a derivative of the way banks engage with them and makes their life easier and better.

Omnichannel Banking Experience: Your online and mobile banking software should not only match but supersede the banking experience drawn at your physical banks. This simply means that the virtual banking experience of your customer should be seamless, personalized, and secured.

Scalability and Flexibility: Your banking application should be able to onboard any number of users and be fit for massive user access at the same time. Cloud adoption is proving to improve efficiency, security, and reduced costs.

IMPACT AREAS OF LEGACY MODERNIZATION

The Way Forward

As the world tunes in to the new normal, the solution to legacy systems is the modernization of core banking systems. Banks looking to enhance their IT efficiency are sorting to innovative technologies of AI/ML, IoT, Cloud Computing, Blockchain, and RPA. The integration of new technologies shall help in unlocking the growth and revenue potentials of banks whilst building a loyal and satisfied customer base. It also enables real-time systems that are agile, scalable, flexible, and cost-effective.

Now is not the time to mull over the prospect of banking legacy software modernization. It is only the survival of the fittest, and to stay fit, banks and financial institutions must weather the storm and adapt to the new rapid evolution of Fintech. This however can’t be a solitary journey!

Get in touch with NeoSOFT’s Application Modernization Experts to get a free consultation towards your first step in the modernization journey.

As organizations adapt to the ongoing COVID-19 crisis, their agile teams can be a real source of competitive advantage. Such teams are typically well suited to periods of disruption, given their ability to adapt to fast-changing business priorities, disruptive technology, and digitization.

Here’s how to ensure they’re effective now that COVID-19 has forced them to work remotely.

1. Sustaining the people and culture of a remote agile team

Remote work for agile teams requires a considerable shift in work culture. It takes a more purposeful effort to create a unified one-team experience, encourage bonding among existing team members, or onboard new ones, or even to track and develop the very spontaneous ideas and innovation that makes agile so powerful, to begin with.

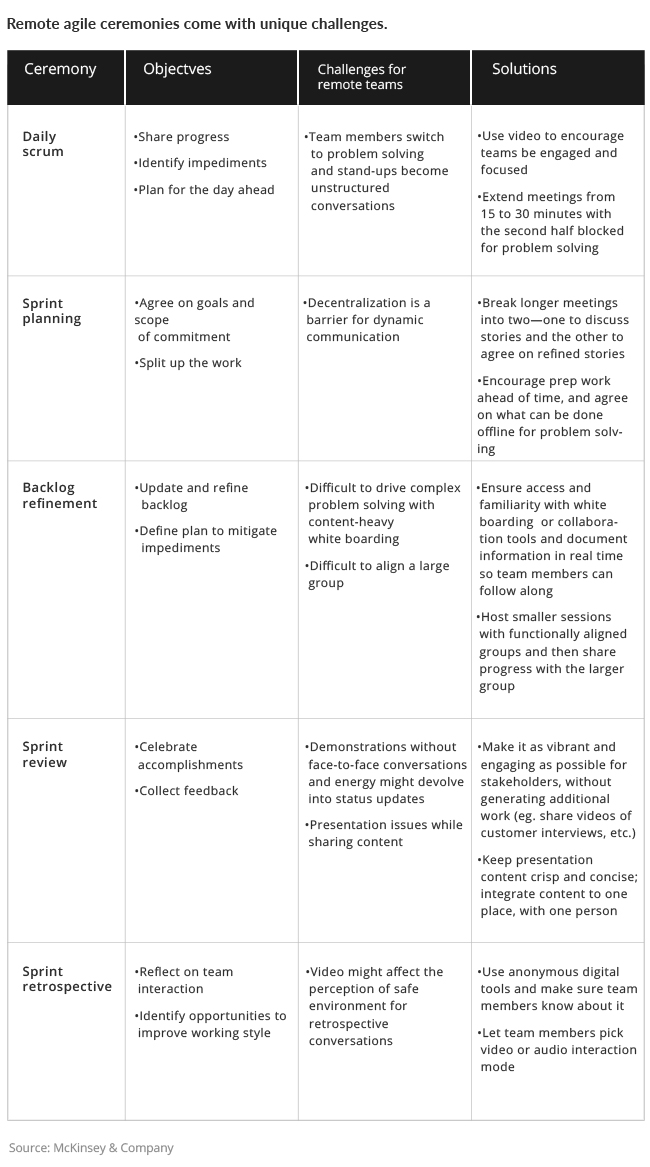

2. Revisit the norms and ground rules for interaction

Virtual whiteboards, instant chat, and videoconferencing tools can be a boon to collaborative exercises and usually promote participation. But they can also require teams to reconsider existing norms and agreed-upon ground rules. Some challenges may require team members to adjust to the tools themselves: team members should be generous with one another in offering practical support on navigating virtual tools—such as help formatting or recording presentations or informing the host about any technology issues. Teams need to get up to speed quickly on visual management and virtual whiteboarding and tailor established ceremonies into standard virtual routines. New ground rules for communication may be needed to keep people who are interacting virtually from talking over one another. Importantly, teams need to be respectful of personal choices. Working from home blurs the lines.

3. Cultivate bonding and morale

Many of the kinds of activities that nurture morale for co-located agile teams—such as casual lunches, impromptu coffee breaks, or after-work social activities—are not possible in a virtual environment. Team members should encourage one another to introduce their pets and family members and to show any meaningful items in their working space. Working remotely, teams need to make a more conscious effort to be social, polite, precise, and tactful—to ensure everyone feels just as safe contributing remotely as they did in person. Agile teams working remotely may also require a more deliberative focus on empathy, openness, respect, and courage.

4. Adapt coaching and development

With coaching, agile teams should aspire to model remotely everything they would have done in person—but more frequently, given the abruptness of the switch to remote format. If you would do one-on-one coaching over coffee, try doing it remotely—while actually having coffee over video. Encourage all team members to turn on their video and actively monitor body language during group meetings, especially those in the role of a coach.

5. Recalibrating remote agile processes

The challenge for remote agile teams is that they’ll be tempted to try to replicate exactly whatever has worked for them in a co-located setting. But what worked in the office setting won’t always work remotely. The trick is to work backwards—start with the outcomes you were getting in the office and modify your scrum ceremonies as appropriate.

6. Establish a single source of truth

Working remotely, teams may need to consider a different approach to documenting team discussion—producing a so-called single source of truth to memorialize agreements. This can then be kept in a single shared workspace. A remote stand-up can be more involved than an in-person one, depending on a team’s cohesiveness and it’s maturity. If team members don’t all participate in the event—or if there’s a risk that they’ll be distracted during the call—then it’s important to calibrate the process to the context. The right approach is likely to be team specific, depending on team maturity and existing norms. Others might find it sufficient to simply submit their notes to a shared online workspace, with a bot to collect and compile everything for the records.

7. Adjust to asynchronous collaboration

Asynchronous communication, such as messaging boards and chat, can be an effective means to coordinate agile teams working remotely. In fact, we have already seen some teams replacing certain traditional ceremonies with asynchronous communication. For example, a team in a services institution has replaced some of the daily huddles by a dedicated messaging channel to which team members submit their updates and identify impediments to further work. This has the benefit of allowing team members to raise red flags at any point during the day, and it serves as the registry of concerns that have been raised and addressed. Note that asynchronous communication needs to be used carefully. Teams that grow overly reliant on asynchronous channels may see team members feeling isolated, and the trust among them may suffer.

8. Keep teams engaged during long ceremonies

A remote-working arrangement creates new challenges in keeping agile teams motivated and avoiding burnout. Working in isolation is hard for any person, but particularly for agile teams accustomed to face-to-face communication and frequent interpersonal engagement. Multitasking and home-based distractions also take a toll, depending on how things are set up. At one US financial institution, for example, a scrum master realized that staring at a video screen for more than a couple of hours was draining without the dynamic interaction of an in-person workshop. Her solution? For longer meetings, she began to schedule in a ten- to 15-minute exercise break every 90 minutes—with a shared videoconference tool to recommend different exercises.

9. Adapting leadership approach

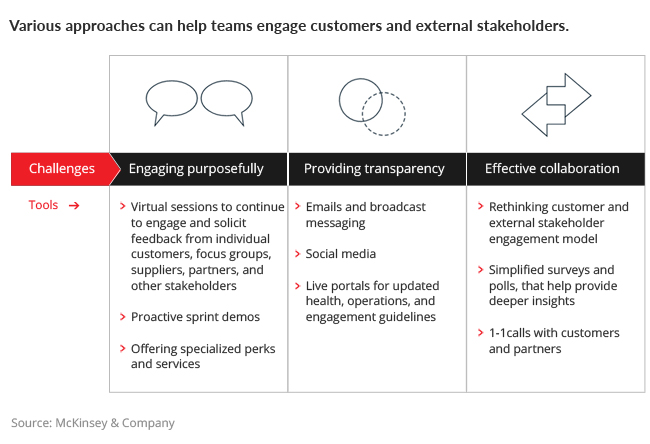

The core mission of leadership stays the same, whether co-located or remote. But leaders need to be more deliberate when engaging with customers and teams, especially when you have limited in-person interaction. Leaders in this context can be anyone on the team, whether product owners, scrum masters, or even a developer demonstrating leadership. They also need to be purposeful at engaging external customers and stakeholders. They must be transparent and reassuring in their communication about team performance and objectives. The tools and approaches can vary. But the individuals and interactions should be the main consideration. Leaders need to show, in their tone and approach, that everyone is in this together.

The abrupt shift to a remote-working environment was a dramatic change that particularly affected agile teams. The hope is that these changes won’t be permanent. But for now, teams can reinforce productivity by taking a purposeful approach to sustaining an agile culture and by recalibrating processes to support agile objectives while working remotely.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.